Other potential causes include changes in technology, raw material costs, and production processes. The more Direct Labor Mix Variance is decreased, the less wasted resources are on production, and the better chance there is that products will be produced within their optimal amount of time. Note that in contrast to direct labor, indirect labor consists of work that is not directly related to transforming the materials into finished goods. Examples include salaries of supervisors, janitors, and security guards. Calculating DLYV is important to assess the productivity of labor and identify areas where operational efficiency can be improved.

Direct labor variance analysis

The direct labor variance measures how efficiently the company uses labor as well as how effective it is at pricing labor. Some production environments report labor over short-term periods by way of a balance sheet that includes total direct labor hours and an estimate of cost, using a standard hourly rate. Rather than formally calculating labor variance, it’s inferred by changes to these amounts compared to a budget and past performance. In this case, the actual hours worked are \(0.05\) per box, the standard hours are \(0.10\) per box, and the standard rate per hour is \(\$8.00\).

Do you already work with a financial advisor?

The labor efficiency variance calculation presented previouslyshows that 18,900 in actual hours worked is lower than the 21,000budgeted hours. Clearly, this is favorable since theactual hours worked was lower than the expected (budgeted)hours. The 21,000 standard hours are the hours allowed given actualproduction. For Jerry’s Ice Cream, the standard allows for 0.10labor hours per unit of production. Thus the 21,000 standard hours(SH) is 0.10 hours per unit × 210,000 units produced.

5: Direct Labor Variance Analysis

After filing for Chapter 11 bankruptcy inDecember 2002, United cut close to $5,000,000,000in annual expenditures. As a result of these cost cuts, United wasable to emerge from bankruptcy in 2006. A financial professional will offer guidance based on the information provided and offer a no-obligation call to better understand your situation. Ask a question about your financial situation providing as much detail as possible. Our mission is to empower readers with the most factual and reliable financial information possible to help them make informed decisions for their individual needs. Our writing and editorial staff are a team of experts holding advanced financial designations and have written for most major financial media publications.

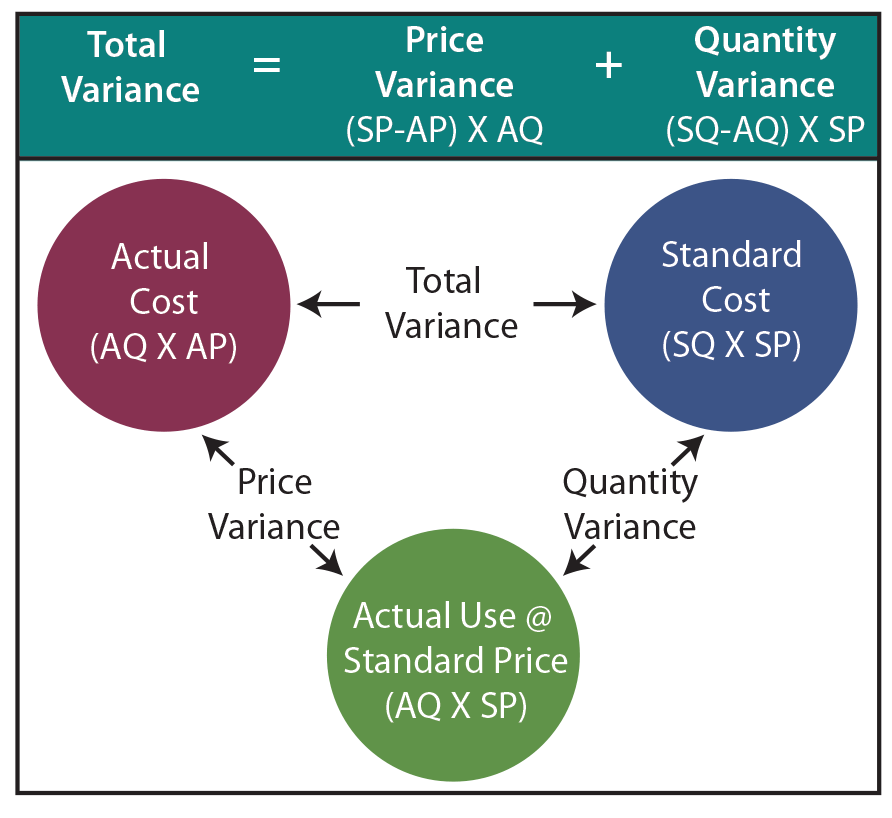

In this case, two elements are contributing to the unfavorable outcome. Connie’s Candy paid \(\$1.50\) per hour more for labor than expected and used \(0.10\) what is the difference between depreciation and amortization hours more than expected to make one box of candy. The same calculation is shown as follows using the outcomes of the direct labor rate and time variances.

Possible Causes of Direct Labor Variances

Usually, direct labor rate variance does not occur due to change in labor rates because they are normally pretty easy to predict. A common reason of unfavorable labor rate variance is an inappropriate/inefficient use of direct labor workers by production supervisors. As with direct materials variances, all positive variances areunfavorable, and all negative variances are favorable. Effective management of labor variance is crucial for maintaining a company’s financial health and operational efficiency. Labor variance, the difference between expected and actual labor costs, can significantly impact profitability and resource allocation. Doctors, for example, have a time allotment for a physical exam and base their fee on the expected time.

- Direct Labor Mix Variance is defined as the difference between the exact amount of labor needed to manufacture a product and the actual amount of labor used for that product.

- Some production environments report labor over short-term periods by way of a balance sheet that includes total direct labor hours and an estimate of cost, using a standard hourly rate.

- Labor efficiency variance downplays the influence of external factors on labor analysis because it uses a standard hourly rate as part of its calculation.

- What if adding Jake to the team has speeded up the production process and now it was only taking .4 hours to produce a pair of shoes?

- This is achieved by subtracting the standard labor rate from the actual labor rate and then multiplying the result by the actual hours worked.

At Finance Strategists, we partner with financial experts to ensure the accuracy of our financial content. For information pertaining to the registration status of 11 Financial, please contact the state securities regulators for those states in which 11 Financial maintains a registration filing. Our Spending Variance is the sum of those two numbers, so $6,560 unfavorable ($27,060 − $20,500). There are several ways Direct Labor Mix Variance can be decreased, but these require training and maintenance of equipment and processes to ensure that they keep working efficiently and the workers need to be motivated. Direct Labor Mix Variance shows how much production is wasted and can be used as a tool to decrease Direct Labor Mix Variance. Textbook content produced by OpenStax is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike License .

Labor efficiency variance downplays the influence of external factors on labor analysis because it uses a standard hourly rate as part of its calculation. A production department may have little ability to control external factors, so labor efficiency variance is an ideal way to analyze changes to labor usage based on factors the department can control. In theory, maximizing production efficiency takes care of itself in the larger picture of overall profitability. In practice, each company can devise its own standard hourly rate, which may not reflect labor levels beyond the scope of internal efficiency. Labor rate variance is the difference between actual cost of direct labor and its standard cost. The difference due to actual amount paid and the standard rate per hour while the time spends during production remains the same.

Calculating labor variance involves a nuanced understanding of both the theoretical and practical aspects of labor cost management. The process begins with establishing standard labor costs, which are derived from historical data, industry benchmarks, and internal performance metrics. These standards serve as a baseline against which actual labor costs are measured. By comparing these two sets of data, companies can identify variances that highlight areas needing attention. Another significant component is labor efficiency variance, which measures the difference between the expected hours of labor required to produce a certain level of output and the actual hours worked. This variance can be influenced by factors such as employee productivity, the effectiveness of training programs, and the efficiency of production processes.

Training employees in these methodologies not only boosts productivity but also fosters a culture of continuous improvement, which is essential for long-term variance reduction. Learn how to manage labor variance effectively with insights on components, calculations, influencing factors, and strategies to optimize financial performance. Hence, variance arises due to the difference between actual time worked and the total hours that should have been worked.